hyperdrive is an algorithmic trading library that powers quant research firm  Algotrade.io.

Algotrade.io.

Unlike other backtesting libraries, hyperdrive specializes in data collection and quantitative research.

In the examples below, we explore how to:

- store market data

- create trading strategies

- test strategies against historical data (backtesting)

- execute orders.

Getting Started

Prerequisites

You will need Python 3.8+

Installation

To install the necessary packages, run

pythom -m pip install hyperdrive -U

Examples

Most secrets must be passed as environment variables. Future updates will allow secrets to be passed directly into class object (see example on order execution).

1. Storing data

Pre-requisites:

- a Polygon API key

- an AWS account and an S3 bucket

Environment Variables:

POLYGONAWS_ACCESS_KEY_IDAWS_SECRET_ACCESS_KEYAWS_DEFAULT_REGIONS3_BUCKET

from hyperdrive import DataSource

from DataSource import Polygon, MarketData

# Polygon API token loaded as an environment variable (os.environ['POLYGON'])

symbol = 'TSLA'

timeframe = '7d'

md = MarketData()

poly = Polygon()

poly.save_ohlc(symbol=symbol, timeframe=timeframe)

df = md.get_ohlc(symbol=symbol, timeframe=timeframe)

print(df)

Output:

Time Open High Low Close Vol

2863 2021-11-10 1010.41 1078.1000 987.31 1067.95 42802722

2864 2021-11-11 1102.77 1104.9700 1054.68 1063.51 22396568

2865 2021-11-12 1047.50 1054.5000 1019.20 1033.42 25573148

2866 2021-11-15 1017.63 1031.9800 978.60 1013.39 34775649

2867 2021-11-16 1003.31 1057.1999 1002.18 1054.73 26542359

2. Creating a model

Much of this code is still closed-source, but you can take a look at the Historian class in the History module for some ideas.

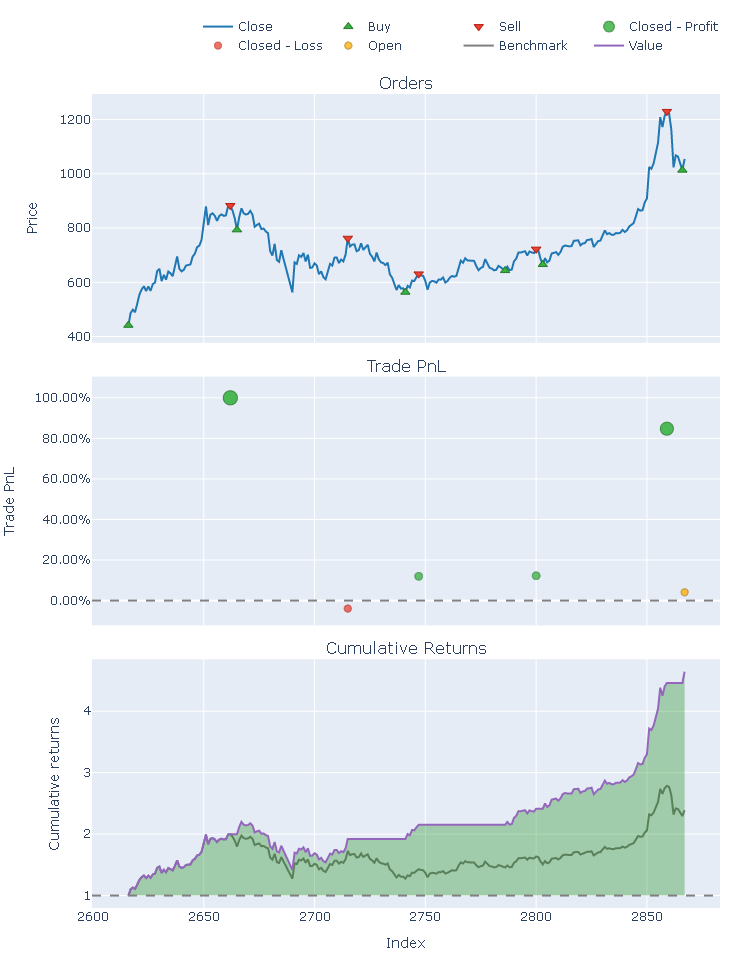

3. Backtesting a strategy

We use vectorbt to backtest strategies.

from hyperdrive import History, DataSource, Constants as C

from History import Historian

from DataSource import MarketData

hist = Historian()

md = MarketData()

symbol = 'TSLA'

timeframe = '1y'

df = md.get_ohlc(symbol=symbol, timeframe=timeframe)

holding = hist.from_holding(df[C.CLOSE])

signals = hist.get_optimal_signals(df[C.CLOSE])

my_strat = hist.from_signals(df[C.CLOSE], signals)

metrics = [

'Total Return [%]', 'Benchmark Return [%]',

'Max Drawdown [%]', 'Max Drawdown Duration',

'Total Trades', 'Win Rate [%]', 'Avg Winning Trade [%]',

'Avg Losing Trade [%]', 'Profit Factor',

'Expectancy', 'Sharpe Ratio', 'Calmar Ratio',

'Omega Ratio', 'Sortino Ratio'

]

holding_stats = holding.stats()[metrics]

my_strat_stats = my_strat.stats()[metrics]

print(f'Buy and Hold Strat\n{"-"*42}')

print(holding_stats)

print(f'My Strategy\n{"-"*42}')

print(my_strat_stats)

# holding.plot()

my_strat.plot()

Output:

Buy and Hold Strat

------------------------------------------

Total Return [%] 138.837436

Benchmark Return [%] 138.837436

Max Drawdown [%] 36.246589

Max Drawdown Duration 186 days 00:00:00

Total Trades 1

Win Rate [%] NaN

Avg Winning Trade [%] NaN

Avg Losing Trade [%] NaN

Profit Factor NaN

Expectancy NaN

Sharpe Ratio 2.206485

Calmar Ratio 6.977133

Omega Ratio 1.381816

Sortino Ratio 3.623509

Name: Close, dtype: object

My Strategy

------------------------------------------

Total Return [%] 364.275727

Benchmark Return [%] 138.837436

Max Drawdown [%] 35.49422

Max Drawdown Duration 122 days 00:00:00

Total Trades 6

Win Rate [%] 80.0

Avg Winning Trade [%] 52.235227

Avg Losing Trade [%] -3.933059

Profit Factor 45.00258

Expectancy 692.157004

Sharpe Ratio 4.078172

Calmar Ratio 23.220732

Omega Ratio 2.098986

Sortino Ratio 7.727806

Name: Close, dtype: object

4. Executing an order

Pre-requisites:

Environment Variables:

from pprint import pprint

from hyperdrive import Exchange

from Exchange import Binance

# Binance API token loaded as an environment variable (os.environ['BINANCE'])

bn = Binance()

# use 45% of your USD account balance to buy BTC

order = bn.order('BTC', 'USD', 'BUY', 0.45)

pprint(order)

Output:

{'clientOrderId': '3cfyrJOSXqq6Zl1RJdeRRC',

'cummulativeQuoteQty': 46.8315,

'executedQty': 0.000757,

'fills': [{'commission': '0.0500',

'commissionAsset': 'USD',

'price': '61864.6400',

'qty': '0.00075700',

'tradeId': 25803914}],

'orderId': 714855908,

'orderListId': -1,

'origQty': 0.000757,

'price': 0.0,

'side': 'SELL',

'status': 'FILLED',

'symbol': 'BTCUSD',

'timeInForce': 'GTC',

'transactTime': 1637030680121,

'type': 'MARKET'}

Use

Use the scripts provided in the scripts/ directory as a reference since they are actually used in production daily.

Available data collection functions: