PyXIRR

Rust-powered collection of financial functions.

PyXIRR stands for "Python XIRR" (for historical reasons), but contains many other financial functions such as IRR, FV, NPV, etc.

Features:

- correct

- supports different day count conventions (e.g. ACT/360, 30E/360, etc.)

- works with different input data types (iterators, numpy arrays, pandas DataFrames)

- no external dependencies

- type annotations

- blazingly fast

Installation

pip install pyxirr

WASM wheels for pyodide are also available,

but unfortunately are not supported by PyPI.

You can find them on the GitHub Releases page.

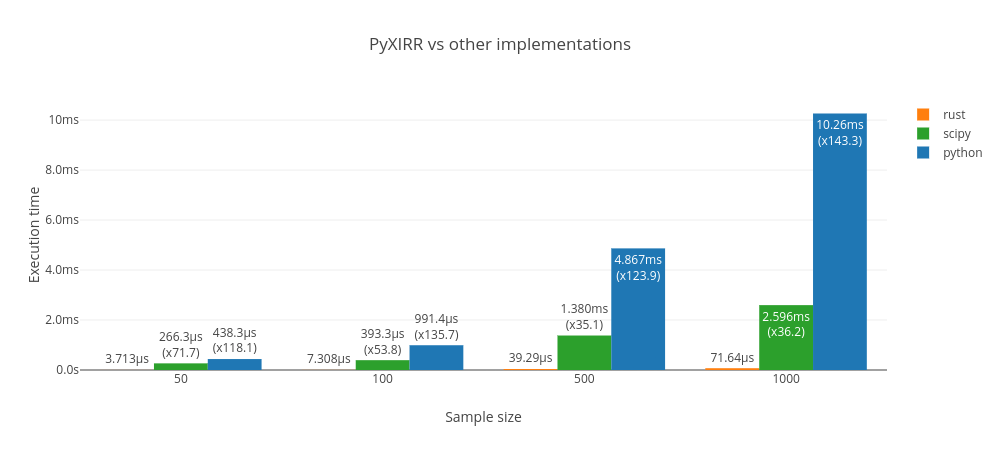

Benchmarks

Rust implementation has been tested against existing xirr package

(uses scipy.optimize under the hood)

and the implementation from the Stack Overflow (pure python).

PyXIRR is much faster than the other implementations.

Powered by github-action-benchmark and plotly.js.

Live benchmarks are hosted on Github Pages.

Example

from datetime import date

from pyxirr import xirr

dates = [date(2020, 1, 1), date(2021, 1, 1), date(2022, 1, 1)]

amounts = [-1000, 750, 500]

xirr(dates, amounts)

xirr(iter(dates), (x / 2 for x in amounts))

xirr(zip(dates, amounts))

xirr(dict(zip(dates, amounts)))

xirr(['2020-01-01', '2021-01-01'], [-1000, 1200])

Multiple IRR problem

The Multiple IRR problem occurs when the signs of cash flows change more than

once. In this case, we say that the project has non-conventional cash flows.

This leads to situation, where it can have more the one IRR or have no IRR at all.

PyXIRR addresses the Multiple IRR problem as follows:

- It looks for positive result around 0.1 (the same as Excel with the default guess=0.1).

- If it can't find a result, it uses several other attempts and selects the lowest IRR to be conservative.

Here is an example illustrating how to identify multiple IRRs:

import numpy as np

import pyxirr

cf = pd.read_csv("tests/samples/30-22.csv", names=["date", "amount"])

print(pyxirr.is_conventional_cash_flow(cf["amount"]))

rates = np.linspace(-0.5, 0.5, 50)

values = pyxirr.xnpv(rates, cf)

print("NPV profile:")

for rate, value in zip(rates, values):

print(rate, value)

import pandas as pd

series = pd.Series(values, index=rates)

pd.DataFrame(series[series > -1e6]).assign(zero=0).plot()

indexes = pyxirr.zero_crossing_points(values)

print("Zero crossing points:")

for idx in indexes:

print("between", rates[idx], "and", rates[idx+1])

for i, idx in enumerate(indexes, start=1):

rate = pyxirr.xirr(cf, guess=rates[idx])

npv = pyxirr.xnpv(rate, cf)

print(f"{i}) {rate}; XNPV = {npv}")

More Examples

Numpy and Pandas

import numpy as np

import pandas as pd

xirr(np.array([dates, amounts]))

xirr(np.array(dates), np.array(amounts))

xirr(pd.DataFrame({"a": dates, "b": amounts}))

xirr(pd.Series(amounts, index=pd.to_datetime(dates)))

df = pd.DataFrame(

index=pd.date_range("2021", "2022", freq="MS", inclusive="left"),

data={

"one": [-100] + [20] * 11,

"two": [-80] + [19] * 11,

},

)

df.apply(xirr)

Day count conventions

Check out the available options on the docs/day-count-conventions.

from pyxirr import DayCount

xirr(dates, amounts, day_count=DayCount.ACT_360)

xirr(dates, amounts, day_count="30E/360")

Private equity performance metrics

from pyxirr import pe

pe.pme_plus([-20, 15, 0], index=[100, 115, 130], nav=20)

pe.direct_alpha([-20, 15, 0], index=[100, 115, 130], nav=20)

Docs

Other financial functions

import pyxirr

pyxirr.fv(0.05/12, 10*12, -100, -100)

pyxirr.npv(0, [-40_000, 5_000, 8_000, 12_000, 30_000])

pyxirr.irr([-100, 39, 59, 55, 20])

Docs

Vectorization

PyXIRR supports numpy-like vectorization.

If all input is scalar, returns a scalar float. If any input is array_like,

returns values for each input element. If multiple inputs are

array_like, performs broadcasting and returns values for each element.

import pyxirr

pyxirr.fv([0.05/12, 0.06/12], 10*12, -100, -100)

pyxirr.fv([0.05/12, 0.06/12], [10*12, 9*12], [-100, -200], -100)

import numpy as np

rates = np.array([0.05, 0.06, 0.07])/12

pyxirr.fv(rates, 10*12, -100, -100)

pyxirr.fv(

np.linspace(0.01, 0.2, 10),

(x + 1 for x in range(10)),

range(-100, -1100, -100),

tuple(range(-100, -200, -10))

)

rates = [[[[[[0.01], [0.02]]]]]]

pyxirr.fv(rates, 10*12, -100, -100)

API reference

See the docs

Roadmap

Development

Running tests with pyo3 is a bit tricky. In short, you need to compile your tests without extension-module feature to avoid linking errors.

See the following issues for the details: #341, #771.

If you are using pyenv, make sure you have the shared library installed (check for ${PYENV_ROOT}/versions/<version>/lib/libpython3.so file).

$ PYTHON_CONFIGURE_OPTS="--enable-shared" pyenv install <version>

Install dev-requirements

$ pip install -r dev-requirements.txt

Building

$ maturin develop

Testing

$ LD_LIBRARY_PATH=${PYENV_ROOT}/versions/3.10.8/lib cargo test

Benchmarks

$ pip install -r bench-requirements.txt

$ LD_LIBRARY_PATH=${PYENV_ROOT}/versions/3.10.8/lib cargo +nightly bench

Building and distribution

This library uses maturin to build and distribute python wheels.

$ docker run --rm -v $(pwd):/io ghcr.io/pyo3/maturin build --release --manylinux 2010 --strip

$ maturin upload target/wheels/pyxirr-${version}*